UK construction output growth eases to six-month low

Total new work rises at slowest pace since June 2024 but business optimism rebounds from 13-month low

UK construction companies indicated a loss of momentum at the end of 2024 with total business activity expanding at the slowest pace since last June, while new order growth moderated for the third month running.

The headline S&P Global UK Construction Purchasing Managers’ Index (PMI) registered 53.3 in December, down from 55.2 in November and the lowest for six months. However, the index has posted above the crucial 50.0 no-change value since March 2024 and the latest reading still signalled a solid upturn in overall construction output.

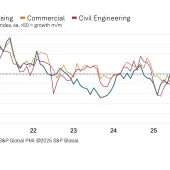

Commercial activity was the fastest-growing area of the construction sector in December (index at 55.0), followed by civil engineering (52.9). That said, both categories saw a slowdown in the rate of business activity expansion since November.

Residential work was again the only category to register an overall decline in output during December (47.6). House-building activity has now decreased for three consecutive months and the latest reduction was the fastest since June 2024. Survey respondents noted that subdued demand conditions, elevated borrowing costs, and weak consumer confidence had all weighed on activity.

Mirroring the trend for output volumes, total new work also expanded at the slowest rate since last June. Anecdotal evidence suggested that improving tender opportunities in the commercial building sector had been offset by cutbacks to residential development projects and a lack of new business to replace completed infrastructure work.

Looking ahead, around 48% of the survey panel predict a rise in output over the course of 2025, while only 15% forecast a decline. The degree of positive sentiment picked up sharply since November, but it was still much weaker than seen in the first half of 2024. While construction firms typically commented on optimism linked to long-term business expansion plans, many also cited worries about the general UK economic outlook and tighter budgets for capital spending.

Tim Moore, economics director at S&P Global Market Intelligence, said: ‘December data highlighted a loss of momentum for construction output growth, with all three main categories of activity posting weaker performances than in the previous month. Commercial building maintained its position as the fastest-growing area of construction activity, followed by civil engineering. In contrast, residential work decreased for the third month running and at the fastest pace since June 2024.

‘The slowdown in overall construction output growth reflected more subdued demand conditions in recent months, as illustrated by a further moderation in new order growth during December. Survey respondents commented on headwinds from elevated borrowing costs and the impact of fragile consumer confidence.

‘Concerns about the demand outlook weighed on construction sector growth expectations for 2025. Although confidence recovered after a post-Budget slump during November, it was still much weaker than in the first half of 2024. Many firms reported worries about cutbacks to capital spending and gloomy projections for the UK economy.’