Gloomy outlook for UK construction

Construction output expected to fall significantly in 2023 amid looming UK economic recession

CONSTRUCTION output is forecast to fall by 3.9% in 2023 following a rise of 2.0% in 2022, as activity currently continues at a high level, according to latest statistics from the Construction Products Association (CPA).

The fall for 2023 is a sharp downward revision from –0.4% in the Lower Scenario of the CPA’s Summer Forecasts. This is mainly due to the impact of a wider economic recession, exacerbated by the effect of the ‘Mini Budget’, and the consequent fallout from recent political uncertainty.

There are still many factors which will adversely affect the construction forecast such as falls in real wages and potential further rises in interest rates, which will likely lead to further falls in consumer spending decisions. On top of these issues, the wider uncertainty around the UK economy means that demand for private housing new build and private housing repair, maintenance, and improvement (RM&I) is expected to fall.

Other key construction sectors, such as commercial and infrastructure, are also expected to be affected by increasing concerns over construction cost inflation, which are likely to hinder project viability.

With an annual turnover of £37 billion, private housing is the largest sector in the construction industry. Activity is currently strong with most major house builders sold through to the first quarter of 2023. However, after the ‘Mini Budget’ announced in October 2022 and the resulting financial market chaos, interest rates are expected to peak at 4%. Activity was already expected to slow due to rising interest rates to 3% but the announcement worsened this forecast.

The repercussions of this on mortgage rates will dampen potential demand and house prices for new homeowners. Furthermore, after more than a decade of low mortgage rates, some existing homeowners will be faced with the pressure of increased mortgage repayments and some may be forced sellers, adding further pressure to the housing market. As a result, property transactions and prices are likely to fall over the next year, with house builders likely to reduce house building targets. After growth of 3.0% in 2022, private housing output is now forecast to fall by 9.0% in 2023 before returning to 1.0% growth in 2024.

Following a record level of £24 billion last year, private housing RM&I output, the third largest construction sector, has been decreasing since March 2022. With a drop in real wages and sharp increases in mortgage payments for many households, there is likely to be a further fall in smaller, discretionary improvements and renovation spending. Output in this sector is expected to decline by 4.0% in 2022 and 9.0% in 2023, before marginal growth of 1.0% in 2024.

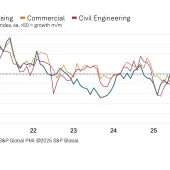

Commercial output is forecast to remain flat in 2022 before a fall of 5.1% in 2023. This comes as buoyant fit-out and refurbishment activity is offset by a hiatus in major new office and mixed-use tower projects, which dominate the sector. Commercial towers are reliant on large, up-front investment for a long-term rate of return.

There are currently major projects in the pipeline over the next 12 months that were signed up to last year. With accelerating costs and worsening economic prospects, however, it raises the question of whether those projects will break ground in the near-term or whether they will be paused and pushed back into 2024 or, potentially even cancelled.

Infrastructure, the second-largest construction sector, should be the least affected by issues of household finances and rising interest rates. Nonetheless, it is not immune to the impacts of both sharp cost increases and government making clear that it will not increase departmental budgets to deal with rising costs. Therefore, we are likely to see the value of activity that we expected previously but not the volume.

In the medium-term, projects towards the end of the Government’s Spending Review will get pushed back into the next review. Councils, which are already financially constrained, are also expected to cut spending on new infrastructure projects and divert finance to cover the rising costs of basic repairs and maintenance. Overall, after 5.2% growth in 2022, infrastructure output is forecast to rise by 1.6% in 2023 and 2.6% in 2024. This will be driven by larger projects already under way, such as HS2, Hinkley Point C, and Thames Tideway, despite the cost overruns and delays.

Overall, given that construction output is expected to fall significantly over the next 12 months, it is critical that new government is focused on delivering its targets including 300,000 net additional homes per year, levelling up, and bringing forward infrastructure activity. Additionally, as part of its movement towards Net Zero, the UK must prioritize the energy efficiency of its new and existing homes.

Professor Noble Francis, economics director at the CPA, said: ‘With the UK economy expected to fall into recession, the construction industry will also fall into a recession. It is worth keeping in mind that activity in the industry currently remains at a historically high level, but it will not be immune to the effects of falling real wages and spending at the same time as the cost of construction continues to rise at double-digit rates.

‘The largest effects will, unsurprisingly, be on private housing and private housing RM&I, given that they are reliant on households’ willingness and ability to spend. Activity in both sectors will fall significantly, albeit from a high point. Major clients’ willingness to invest in new commercial developments will also be tested given concern over the UK economy and rising construction costs. Furthermore, infrastructure will be adversely affected by central government and local authority spending constraints as well as increased pressure for austerity despite continual government announcements and reannouncements of more and more infrastructure.’